Cash Advance Explained: Demystifying Short-Term Loan Solutions

The Ins and Outs of Loans: Navigating Your Funding Selections With Confidence

Maneuvering the facility landscape of loans needs a clear understanding of different types and necessary terms. Several people locate themselves bewildered by alternatives such as personal, car, and student loans, in addition to vital principles like rates of interest and APR. An understanding of these principles not just help in reviewing economic needs yet likewise boosts the loan application experience. There are significant aspects and usual mistakes that debtors need to identify before proceeding further.

Recognizing Various Types of Loans

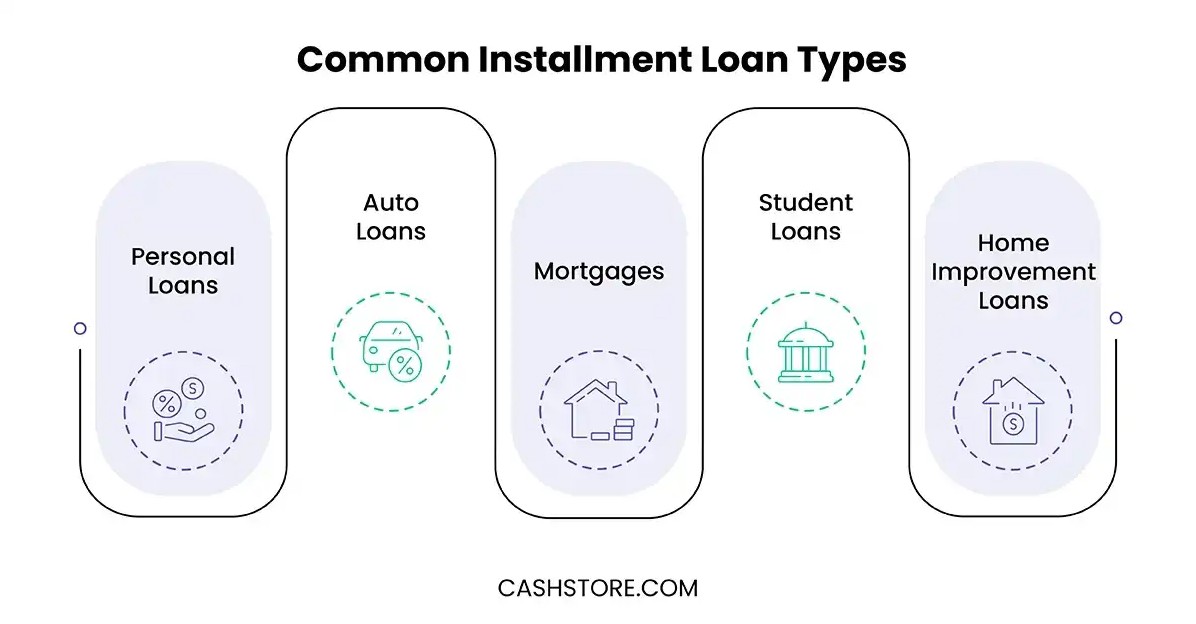

Loans function as vital economic devices that satisfy various needs and objectives. Businesses and people can choose from numerous kinds of loans, each designed to meet particular needs. Individual loans, typically unsecured, give borrowers with funds for numerous personal expenses, while auto loans make it possible for the acquisition of automobiles through safeguarded funding.

Home loans, or home loans, aid customers in obtaining building, typically involving lengthy payment terms and specific passion rates. Student loans, targeted at moneying education, often included lower rates of interest and deferred settlement choices till after graduation.

For services, commercial loans provide needed resources for expansion, equipment purchases, or functional costs. Additionally, payday advance offer quick cash money services for immediate requirements, albeit with higher rate of interest. Understanding the various kinds of loans enables consumers to make informed decisions that line up with their economic goals and situations.

Key Terms and Concepts You Should Know

When steering loans, recognizing vital terms and principles is essential. Rates of interest play an essential role in figuring out the cost of borrowing, while different loan types deal with numerous monetary needs. Knowledge with these components can encourage people to make educated choices.

Rate Of Interest Described

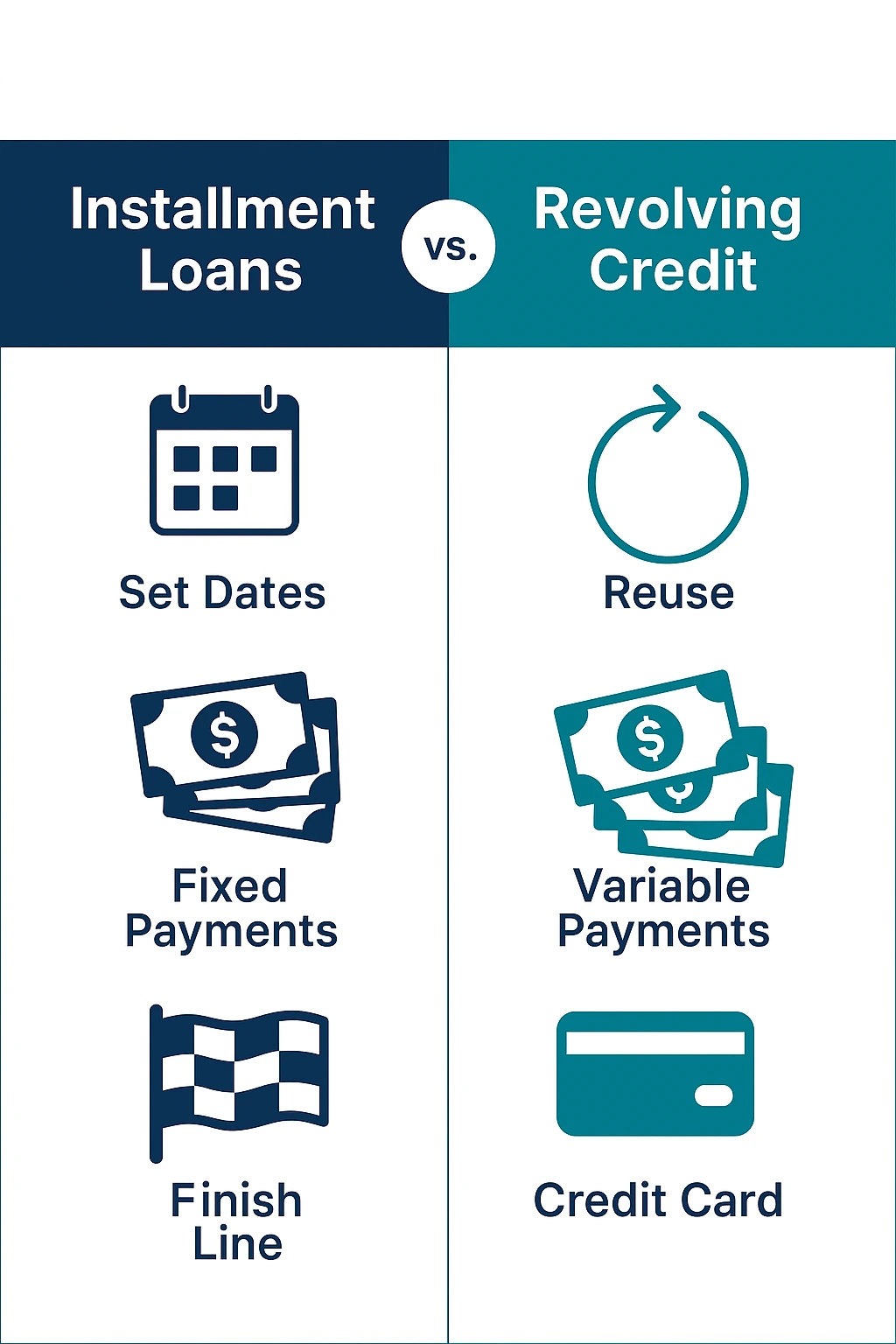

Just how do rates of interest effect loaning decisions? Interest rates represent the expense of obtaining money and are a vital consider monetary decision-making. A higher rate of interest raises the overall cost of a loan, making loaning much less attractive, while reduced rates can incentivize consumers to tackle financial obligation. Lenders usage rates of interest to reduce danger, reflecting borrowers' creditworthiness and dominating financial problems - Installment Loans. Dealt with rates of interest stay continuous throughout the loan term, providing predictability, whereas variable rates can fluctuate, possibly bring about higher settlements over time. Furthermore, comprehending the yearly portion price (APR) is vital, as it includes not simply interest however likewise any linked charges, offering a detailed sight of borrowing prices

Loan Enters Review

Maneuvering the landscape of loan kinds is essential for borrowers seeking the most appropriate funding choices. Understanding various loan types assists individuals make notified decisions. Individual loans are usually unsafe, suitable for settling debt or funding personal jobs. Mortgages, on the various other hand, are protected loans specifically for acquiring realty. Auto loans offer a comparable purpose, funding automobile purchases with the lorry as security. Service loans deal with business owners requiring capital for operations or expansion. Another option, student loans, assist in covering academic expenses, usually with positive repayment terms. Each loan type provides distinct terms, rates of interest, and eligibility requirements, making it necessary for consumers to analyze their financial needs and abilities prior to devoting.

The Loan Application Refine Explained

What actions must one take to successfully browse the loan application procedure? Individuals ought to examine their economic demands and identify the type of loan that aligns with those requirements. Next, they ought to evaluate their debt record to validate accuracy and recognize locations for improvement, as this can influence loan terms.

Following this, consumers need to gather essential documents, including proof of earnings, work background, and financial statements. Once prepared, they can approach lenders to make inquiries concerning loan products and passion rates.

After picking a loan provider, finishing the application form precisely is necessary, as omissions or errors can postpone processing.

Applicants should be all set for prospective follow-up requests from the lending institution, such as additional documentation or explanation. By complying with these actions, people can boost their possibilities of a smooth and reliable loan application experience.

Elements That Impact Your Loan Approval

When thinking about loan approval, a number of essential factors come right into play. 2 of one of the most considerable are the debt rating and the debt-to-income proportion, both of which supply loan providers with understanding right into the borrower's financial security. Understanding these elements can greatly enhance an applicant's chances of protecting the wanted financing.

Credit Score Relevance

A credit score serves as an essential criteria in the loan approval process, influencing loan providers' understandings of a borrower's financial dependability. Generally varying from 300 to 850, a greater score shows a background of liable credit report use, including timely repayments and low debt utilization. Various variables add to this rating, such as repayment background, size of credit report, kinds of credit accounts, and recent credit scores queries. Lenders make use of these ratings to evaluate danger, determining loan terms, rate of interest rates, and the likelihood of default. A solid credit rating score not just boosts authorization possibilities yet can likewise result in extra desirable loan problems. On the other hand, a reduced rating might result in greater rate of interest rates or denial of the loan application entirely.

Debt-to-Income Ratio

Numerous lenders consider the debt-to-income (DTI) ratio a vital element of the loan approval procedure. This financial statistics contrasts an individual's monthly financial debt settlements to their gross monthly earnings, offering understanding right into their capability to take care of extra financial obligation. A lower DTI ratio shows a healthier economic circumstance, making debtors extra appealing to lending institutions. Aspects affecting the DTI ratio consist of real estate expenses, bank card equilibriums, trainee loans, and other persisting expenditures. Additionally, modifications in revenue, such as promotions or job loss, can substantially influence DTI. Lenders usually like a DTI proportion listed below 43%, although this limit can vary. Handling and understanding one's DTI can improve the possibilities of securing desirable loan terms and rate of interest.

Tips for Handling Your Loan Sensibly

Typical Errors to Prevent When Taking Out a Loan

Furthermore, several individuals hurry to accept the first loan deal without comparing choices. This can lead to missed opportunities for better terms or lower rates. Borrowers should likewise stay clear of taking on loans for read more unnecessary expenditures, as this can result in long-lasting financial debt troubles. Ultimately, ignoring to assess their credit rating can impede their ability to secure positive loan terms. By recognizing these mistakes, customers can make educated choices and navigate the loan process with better self-confidence.

Regularly Asked Concerns

Exactly How Can I Enhance My Credit Score Prior To Getting a Loan?

To enhance a credit score before making an application for a loan, one must pay bills on schedule, reduce arrearages, examine credit scores reports for mistakes, and prevent opening brand-new credit accounts. Regular monetary behaviors generate favorable outcomes.

What Should I Do if My Loan Application Is Rejected?

Exist Any Type Of Costs Related To Loan Prepayment?

Funding early repayment costs might use, depending on the loan provider and loan kind. Some loans include charges for very early settlement, while others do not. It is necessary for borrowers to examine their loan agreement for details terms.

Can I Bargain Loan Terms With My Lender?

Yes, debtors can negotiate loan terms with their lending institutions. Factors like credit history, settlement background, and market conditions may influence the loan provider's willingness to change rates of interest, payment schedules, or fees related to the loan.

Just How Do Rate Of Interest Rates Affect My Loan Settlements Gradually?

Rate of interest rates substantially influence loan payments. Greater rates cause boosted regular monthly payments and overall interest prices, whereas lower prices reduce these expenses, inevitably impacting the borrower's overall monetary concern throughout the loan's duration.

Lots of individuals locate themselves bewildered by choices such as personal, vehicle, and pupil loans, as well as crucial ideas like interest rates and APR. Interest rates play an important function in figuring out the cost of borrowing, while various loan types cater to numerous financial requirements. A greater rate of interest rate enhances the total price of a loan, making borrowing less enticing, while reduced rates can incentivize consumers to take on debt. Dealt with interest rates continue to be constant throughout the loan term, providing predictability, whereas variable prices can rise and fall, potentially leading to greater payments over time. Lending early repayment costs might apply, depending on the loan provider and loan kind.